Berkeley Mineral Resources running low on cash as Zambian tailings project approval continues to be delayed

Mar 28, 2014 at 1:28 pm in AIM by contrarianuk

Just when I was thinking it was only AIM oil and gas that was cursed by bad news and lack of transparency, the turmoil at Berkeley Mineral Resources (BMR) caught my eye. BMR is focused on developing the extraction of Lead and Zinc from tailings deposits at former mines in Northern Zambia.

Its lead project is at the Kabwe Zinc and Lead mine which was in operation from 1906 until 1994 and produced some nearly 3 million tonnes of Zinc and Lead in the 88 years of mining. Berkeley has always been the focus of much private investor interest with heavy speculation relating to its key Kabwe project and the start of tailings processing following approval by Zema, the Zambian mining regulator. The web site for the company says that the start of processing was expected in late 2013 but this has slipped due to ongoing environmental consultations. The Company’s above-ground tailings at EPL’s Kabwe site comprise an estimated 6.4 million tonnes of zinc and lead with an estimated 708,000 tonnes of contained metal plus other valuable minerals. The Kabwe underground mine contains an additional estimated 51 million tonnes of ore at an average combined grade of 4.01%.

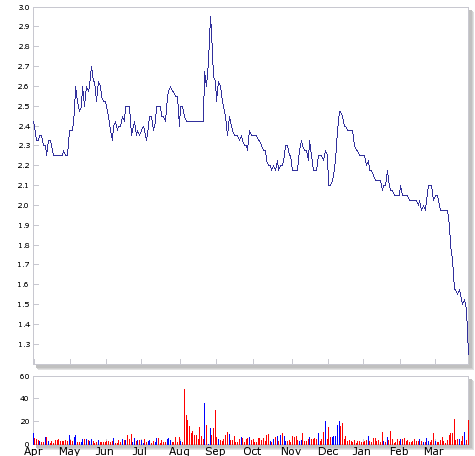

The company is led by Masoud Alikhani who is Chairman and Executive director and like Cole, Hart, Kozel in the oil sector, the focus of much private investor derision right now following today’s announcements. This week the shares have slumped some 20% and today alone 15% on the release of the company’s interim results. They are currently changing hands for 1.25p giving a market cap of just shy of £15 million.

The key worry for investors are the dwindling cash in the bank given the delays with Zema and the Kabwe project. This mornings RNS said that “Since the start of 2014, ZEMA has continued to review EPL’s ESIA submission. It has scheduled a public meeting in Kabwe for April 11th 2014.” Even if the operation does get off the ground offtake agreements still haven’t been signed, “The Company has received significant interest from international parties seeking to enter into an off-take agreement. These discussions are continuing.”. It seems surprising that given the amount of time the company has had to nail down these off take agreements, the management team hasn’t managed to get a contractual agreement.

The loss for the six months to the end of December was £0.88 million, up from £0.59 million last time, with the cash balance at the period end being £0.40 million compared with £0.30m at 30 June 2013.

The really disappointing piece of news came with an announcement relating to warrants in the company. “On 5 August 2013, the Company changed the exercise price of 127,916,666 warrants (exercisable until 24 October 2013) from 6p to 2p to be exercised by institutional investors. On the 9 August 2013, the terms of the remaining 72,500,000 warrants exercisable before 28 June 2014 were amended to reduce the exercise price from 6p to 2p and reduce the exercise period to 24 October 2013. On 23 October 2013, the exercise period of the remaining warrants was extended from 24 October 2013 to 24 January 2014. During the period under review a total of 82,662,897 warrants were exercised, raising £1,653,258 before expenses. On 2 January 2014, a further 3,147,149 warrants were exercised, raising £62,943 before expenses. On 24 January 2014, the exercise period of the remaining 114,606,620 were further extended from 24 January 2014 to 24 April 2014. On 28 January 2014, 2,045,645 warrants were exercised raising £40,913 before expenses and on 3 February 2014, 670,000 share options were exercised at 1p per share, raising £6,700. The Board has agreed that the remaining 112,560,975 outstanding warrants exercise price of 2p be reduced to 1.25p.”

So the company now has nearly 113 million warrants outstanding at 1.25p which is the current market price, therefore it is unlikely that institutional investors will take them up unless their price is further reduced.

A sorry state of affairs with plenty of further pressure on the shares until the Zema approval comes through, presumably by the summer of 2014. At least “the Company has sufficient resources to continue to meet its obligations as they fall due.” but a caveat “However in order to advance all of the projects the Company will need to raise additional funds. The Company remains in negotiations for off-take arrangements with a number of interested parties.” So BMR needs more cash and where will this come from? This feels very much like Greenland focused miner, Angel Mining, which unfortunately came a cropper in 2012 when a key lender called in the loan.

An ultra low share price means that an equity placing would be disastrous, but perhaps the company can strike a deal with one of its partners. On 10 December 2013 the Company announced the signing of a Strategic Cooperation Agreement with a Chinese group, Hunan Nuclear Geological Bureau (“HNGB”), a company located in Hunan Province, Peoples Republic of China. If HNGB do swoop in to help BMR it will probably not be on terms particularly advantageous to BMR shareholders given that BMR has only £400,000 left in cash.

Bottom fishing this one looks pretty risky after all the false dawns of the past.

Contrarian Investor UK

IMPORTANT: The posts I make are in no way meant as investment suggestions or recommendations to any visitors to the site. They are simply my views, personal reflections and analysis on the markets. Anyone who wishes to spread bet or buy stocks should rely on their own due diligence and common sense before placing any spread trade.