Further controversy stalks Quindell

Jun 12, 2014 at 9:23 am in AIM by contrarianuk

AIM listed Quindell is never far from controversy right now with the company’s shares plummeting by 25% at one point yesterday and down a further 9.5% today on news relating to the rejection of its main market listing. Since April investors have had a sinking feeling that’s for sure!

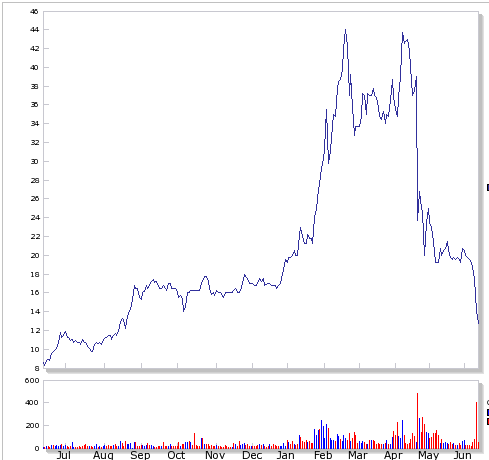

The company first floated in May 2011 and has grown aggressively over the last few years as a result of an acquisition with sales revenue increasing from £13.7 million at the end of 2011, to £380 million by the end of 2013. The shares have had a tremendous run up in 2012, 2013 and early 2014, before plummeting in late April 2014.

It began as a golf and country club but is now focused on the insurance claims handling sector, providing services like car repairs and legal services. It is also using technology like telematics that monitor driver behavior and offer the potential to cut premiums and recently announced an agreement with the RAC to form a venture called Connect Car Solutions. Quindell has made about 30 acquisitions of legal, medical and other companies since 2011 and tapped investors for around £300 million to fund these deals.

The RNS released yesterday morning read as follows,

“Quindell Plc (AIM: QPP.L), the provider of sector leading expertise in software, consultancy and technology enabled outsourcing in its key markets, being Insurance, Telecommunications and their related sectors, is today providing a further update on its proposed move to a Premium Listing on the Main Market.

As previously announced, the Company’s advisers have been engaged regarding a move to the Premium List of the Main Market. Considering the significant growth of the Group in recent years the Company has today been advised that it has not been able to satisfy Listing Rule 6.1.3 at this time, and particularly, the criteria in Listing Rules Guidance Note 6.1.3E (5) which states that an applicant may not be eligible if its business has undergone a significant change in its scale or operations during the period of the historical financial information, being the last three years’ audited accounts.

The Company and its advisers continue to believe that the Premium List is the optimum UK market for the Company and will continue to seek a listing on this market as soon as practicable. The Company will also continue to explore other options, including listing in North America.”

Quindell is the first company quoted on the Alternative Investment Market to be turned away publicly by the UK Listing Authority and is a major disappointment for shareholders. Rob Terry, founder and executive chairman is a man with plenty to worry about right now after this latest piece of news. The company could be a victim of its own success given the huge growth which may well have frightened away the Listing Authority as reported by the RNS but of course yesterday’s fall in the share price is both a reflection of disappointment and perhaps concern that things may be not what they seem as others have alleged.

The latest revelation from Quindell comes about a damning report from Gotham City Research questioning the company’s business model back in April. Before this the company admitted in May 2013 it was funding expansion through an equity-swap deal which hit the shares hard at the time.

The rejection of Quindell’s efforts to move to the main market relate specifically to caluse 6.1.3 (5) of the listing regulations and the clause reads as follows:

The purpose of LR 6.1.3B R is to ensure that the issuer has representative financial information throughout the period required by LR 6.1.3R (1)(a)and to assist prospective investors to make a reasonable assessment of what the future prospects of the new applicant’s business might be. Investors are then able to consider the new applicant’s historic revenue earning record in light of its particular competitive advantages, the outlook for the sector in which it operates and the general macro economic climate. The FCA may consider that a new applicant does not have representative historical financial information and that its equity shares are not eligible for a premium listing if a significant part or all of the new applicant’s business has one or more of the following characteristics:

(1) a business strategy that places significant emphasis on the development or marketing of products or services which have not formed a significant part of the new applicant’s historical financial information;

(2) the value of the business on admission will be determined, to a significant degree, by reference to future developments rather than past performance;

(3) the relationship between the value of the business and its revenue or profit-earning record is significantly different from those of similar companies in the same sector;

(4) there is no record of consistent revenue, cash flow or profit growth throughout the period of the historical financial information;

(5) the new applicant’s business has undergone a significant change in its scale of operations during the period of the historical financial information or is due to do so before or after admission;

(6) it has significant levels of research and development expenditure or significant levels of capital expenditure.

Gotham issued a 74 page report alleging the shares were worth no more than 3p. Within minutes of the report being issued the shares had fallen by over 50% to 18p and finished the trading day down 39% at 23p. Gotham claimed that between 42% and 80% of Quindell’s profits being “suspect” with it being “little more than a country club until 2008/2009, yet Quindell somehow began reporting Microsoft/Google-esque profit margins in 2010/2011”. Gotham said that 41% of 2011 revenues came from an “undisclosed related party controlled by a Quindell executive” and that between 26-43% of the company’s revenues come from subsidiary Clickus4.com, with over ten acquisitions having no “economic substance”.

Quindell fought back claiming the note was defamatory and misrepresentative and a deliberate effort by Gotham to make money by shorting the shares but the damage was done and confidence clearly bruised. Doubts about the Quindell business model were planted in investors minds, even if the allegations were right or wrong.

The company is now valued at £788 million, with the shares at 12p, versus a 52 week high of 44p hit in early April before the Gotham accusations. Quindell is a “hold onto your hats” sort of share that’s for certain. What else has Rob Terry got up his sleeve to repair the battered sentiment of this share? Things have come down a long way in the last 2 months, a contrarian bet? Perhaps, but certainly not for the faint hearted!

Contrarian Investor UK

IMPORTANT: The posts I make are in no way meant as investment suggestions or recommendations to any visitors to the site. They are simply my views, personal reflections and analysis on the markets. Anyone who wishes to spread bet or buy stocks should rely on their own due diligence and common sense before placing any spread trade.