Q. What is a carry trade?

A: This is a classic forex trading strategy which works better in times of low volatility. The trading strategy revolves around buying a high yielding currency while shorting a low yielding one and then pocket the difference in the process. A carry trade is when a trader borrows from a currency where the interest rate is low, such as US dollars and then converts it into a higher yielding currency such as the Australian $ (AUD/USD). The difference is called the carry. The carry trade trading strategy involves selling a low-yielding currency to fund the purchase of a high-yielding one.

Trading a forex pair is akin to buying the currency of one country, and selling that of another. When you buy the AUD/USD pair you are effectively lending Australian dollars at an annual interest rate of close to 4.75% and borrowing USA dollars at a yearly annual rate of about 0.2%. All things equal, if the AUD/USD exchange rate remains stable you will end up earning an income equivalent to the interest rate differential between the two currencies (about 4.55%) a year. Make this work with leverage through a spreadbet and the end return would be even more attractive. However you need to consider that each country sets its own interest rates that it pays on money, and there are, of course, not only wide disparities among the nations of the world, but everybody’s rates are changing all the time. In our AUD/USD pair example, the carry trade strategy would be even more profitable if the Australian dollar were to rise in value against the USA dollar (but of course the converse is also true)

Now, whenever you buy the currency of one country, you effectively own that money, and you are entitled to receive interest on it at the going rate. Conversely, if (or when) you sell short the currency of another country, you actually are ‘giving away’ their money, and you are obligated to pay interest on it as well (at whatever rate that country charges). As an example, if I were to go long the Dollar-Yen Forex pair, I am actually buying U.S. dollars and selling Japanese yen. And I would be entitled to collect interest on my Dollars at whatever interest rate the United States Government happens to be paying. And at the same time, I would be obliged to pay interest on the Yen to whomever I sold it to, at whatever rate the Bank of Japan happens to be paying on its money. Since Forex trading always involves the simultaneous buying of one currency while selling another, this situation always exists to some degree on every trade that we ever make.

The carry trade strategy is an attempt to profit from the interest-rate differential between two currencies. It involves borrowing and subsequently selling a low-interest currency to fund the purchase of a higher-yielding currency. Usually, the higher yield currency will also appreciate which means that the spread trader will end up with the benefit of a a positive carry by owning the higher rate currency, and subsequently lending it, while only paying a small borrowing cost in funding the sold currency.

A forex holding earns the rate of interest of the currency you have lent and incurs the rate of the one you have borrowed. The net difference is credited or debited to or from your account each night the position is rolled over. This is automatically calculated by your forex provider using the overnight lending and deposit rates.

Now, when I say that I am entitled to collect interest on the currency I own and required to pay interest on the currency I sell, the question arises: who is on the other side of the trade? Who pays me the interest that I am entitled to, and to whom do I have to pay out interest on the money that I sold? And without getting into the legal aspects of international counterparty financial transactions, the answer is that it’s your brokerage firm which both pays and collects this interest.

For every day that you hold a position, your brokerage firm will look at which currency you are long, and will pay you interest on your money, and they will also look at which currency you are short, and will charge you interest on that money. And simply depending on which country has the higher interest rates, you will either make or lose money on this deal.

The decade-long slump by the dollar has been partially fed by economic policy, according to Gurjit Dehl, economist at consulting firm Redington and former currency and rates trader.

‘Before the 2001 crisis and a sharp drop in US interest rates (which fell from 6.25% in 2001 to 1% in 2003), this ‘carry trade’ was dominated by investors borrowing in yen,’ said Dehl. ‘The extended period of low US rates between 2001 and 2004 encouraged investors to switch to borrowing the dollar at cheaper rates in order to invest in their home market or higher yielding foreign countries. ‘This also saw the Swiss franc and euro being used to finance investments in countries with higher borrowing costs, including Eastern Europe, Asia and South America.’

A note to investors everywhere, however, is that this trade also helped to secure Iceland’s demise in 2008 as Icelanders and their banks had borrowed not in their national currency – the krone – with an interest rate several per cent higher than Japan, Switzerland, US and Europe, but in yen, franc, dollar and euro. The ensuing economic boom was short-lived as foreign investors spotted a bubble and froze lending to the country, forcing Icelanders to sell their own assets to repay those loans, just as their currency dropped in value by more than 50% against those currencies. This turned a bad dream into a nightmare.

For instance at the time of writing (Nov 2010) forex traders are looking at shorting the dollar with a view to buying in currencies such as the Australian dollar or New Zealand dollar, both of which enjoy a sufficient interest-rate differential for the carry trade to work.

Note that the carry trades works better during periods of reduced volatility since a carry trade needs to be run over an extended period of several months to result in tangible gains. Volatility kills the carry trade. Economic uncertainties and financial crisis could create volatility that might easily wipe out any gains a carry trader would have stood to make out of the interest-rate differential.

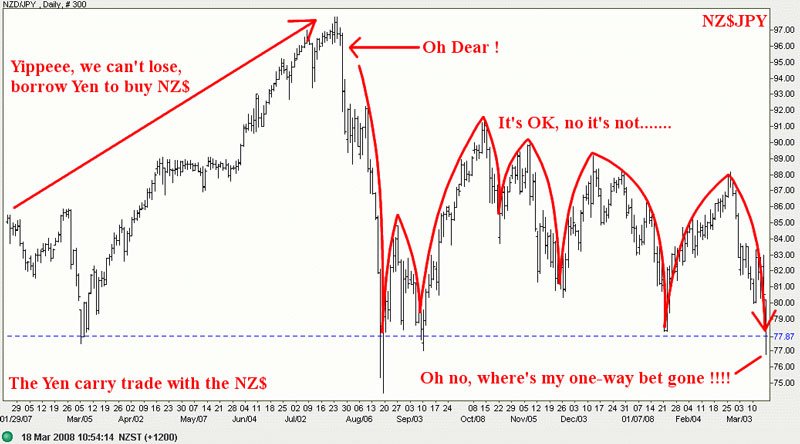

This is my take on the JPY to NZ$ carry trade, which pretty much sums up all of them with the Yen

|